Positive outlook for east/central European steel: Executives

The steel industry in central and eastern Europe is set to see continued support from positive economic growth in 2018, executives at the EUROMETAL regional conference in Vienna said Tuesday.

In 2017 economic growth in the central and east European region was positive. Regional growth is to remain strong this year, but a modest slowdown is expected going forward.

Analysts expect the region’s economy to expand by 3.6% in 2018, led by higher GDP forecasts in Romania (4.2%), Poland (3.8%), Hungary (3.5%), Czech Republic (3.2%) and Croatia (2.8%).

“In 2018 [the steel industry] will still be ok, but we are cautious that this might not be sustainable. We hope there won’t be a drop, but there might be a slowdown. We are prepared to use the brakes,” said Jan Moravec, corporate audit manager at Ferona.

The outlook for steel demand in 2018 is also good, with some positive demand indicators seen in large steel-consuming sectors, such as construction and automotive, speakers said. However, there are risks around reduced EU funding in the longer term, partly affected by Brexit.

Car production is expected to grow by over 20% in the next five years, while construction is seen growing by over 23% in the next three years, noted Gabriel Holub, sales manager at US Steel Kosice.

“The construction industry is currently in a rather comfortable position, with a favourable outook for 2018,” said Michael Weingartler, Construction Market and Housing Policy Expert at Eurocontruct. “Solid economic growth in the EU supports positive outlook for construction and output should increase

4% in east and central Europe in 2018, with Poland, Hungary and Czech Republic leading the growth.”

Erica Sesay, PLATTS

Steel flats imports would be most impacted by EU safeguard

Flat products imports will take the main hit from the EU’s safeguard investigation into steel imports launched in reaction to the declaration of US tariffs on steel (25%) and aluminum (10%), including against the EU, according to Georges Kirps, the head of EUROMETAL.

Speaking at a regional meeting in Vienna on Tuesday, Kirps noted that import volumes of flat products into the EU market last year were 20.3 million and accounted for 69% of the total volumes under the safeguard investigation. By comparison, longs and tubular products volumes were respectively 6.4 million mt and 2.7 million mt, or 22% and 9% of the total.

All product categories under investigation represent 18% of the EU steel supply chain.

According to Gabriel Holub, a representative of Slovakian flats steel producer US Steel Kosice, owned by the US Steel group, said Section 232 represented the main downside risk for the European market as it will likely lead to similar measures taken by other countries. But at the same time the EU safeguard measures, if adopted, should help to protect the EU market against massive inflow of material from other regions blocked by the US, he added.

A member of the trading community at the meeting called the current safeguard procedure in the EU a “very difficult situation” for independent service centers, traders and distributors, who are depending on imported material beside the material they buy from the EU mills.

“There has to be a healthy mixture between both otherwise we lose our competitive edge,” he said. “We need to have the opportunity to buy right and left and not just from two big mills in Europe controlling 70% of the market.

Wojtek Laskowski, PLATTS

Independent SSC future seen bright, protectionism a threat

Independent service centres have a bright future as they are able to tailor services to the needs of individual customers better than mills and can offer more competitive pricing. This was the opinion among the majority of participants at the Central Europe Regional Meeting of Distributors’ association EUROMETAL.

During the panel discussion, Czech service centre Mi-King SSC general manager Garry Furey said besides being able to service smaller customers, distributors can also offer non-EU material. “We provide something to non-EU mills because we give them the ability to sell in Europe and not let down their customers in Europe,” he said at Tuesday’s meeting in Vienna attended by Kallanish. Moreover, distributors are able to operate in the local language of the countries they are based in.

As a tube producer, Branimir Minchev of Bulgaria-based Steelimpex agreed that service centres and distributors better cater for small-tonnage orders and specific requirements. Steelimpex conducts back-to-back business as it does not want to store purchased hot and cold rolled coil for a longer period so that it is not damaged, he said. The firm therefore prefers to sell small tonnages to stockholders for processing.

Jan Moravec, executive director – corporate audit at Czech distributor giant Ferona, said mill-tied distributors can be inefficient. “These (mill-tied) distribution networks are basically forced to follow certain strategies and they are not flexible enough,” he opined. These distributors are not able to purchase from a wide selection of sources and may therefore not offer the optimal product, he added.

“I also think the future is independent centres,” Minchev responded. These firms are “…much more flexible, they can buy from everywhere, they can deliver different material and they are able to… find the best price.” Moreover, local service centres can reduce risk for foreign companies selling into individual countries, he added.

An opposing view was, however, offered by Roland Fazekas, president of Hungarian stockholder Carboferr. “I don’t think independent service centres have that bright a future,” he warned. “We can see it in the anti-dumping procedures: it was a fight between integrated mills and independent players on a large scale… and we could see that now it’s really in the favour of integrated.”

Mills have moved more into stockholding in recent years due to the zero interest rate environment that makes it easier to keep stock and serve smaller customers, Fazekas said. This will only change when interest rates rise and mills are forced to return to traditional means of financing, he added.

Ralf Reintjes, managing director of German trader Primex Steel and ISTA executive committee member, said “…independent service centres are the backbone of the industry.” However, they are in danger due not only to the anti-dumping measures but also to the EU’s safeguard probe launched in response to Section 232, which is a “…general attack on imports.”

“There should be a certain structure on the import side, we should not have a Wild West market,” Reintjes continued. “All the independent traders, service centres, distributors are depending on imported material besides the material they buy from EU mills. There has to be a healthy mixture between both, otherwise we lose our competitive edge.” Distributors need a body independent of Eurofer to represent them in EU trade cases, he suggested.

Central European distributors fear market correction

There is likely to soon be a reduction in steel consumption and prices in Central and Eastern Europe as the market is overheated after an “…extremely good” 2017. So said Jan Moravec, executive director – corporate audit at Czech distributor giant Ferona, during Tuesday’s Central Europe Regional Meeting of Distributors’ association EUROMETAL.

“2018 will still be ok, but we are extremely nervous – if we do not perform, we are nervous, and if we perform too much we are nervous as well because it’s not sustainable,” Moravec said during the panel discussion at the meeting in Vienna attended by Kallanish.

“We really think we are on the top, I mean the V4 countries… We hope there will be no drop, but there will be a certain slowdown and definitely a certain reduction, but of course no one knows when,” he continued. US tariffs have clouded the situation further.

Roland Fazekas, president of Hungarian stockholder Carboferr, added: “We could see very nice figures for the construction market… for Hungary and Poland, but we already see the price correction in the rebar market, for example, and in terms of demand the past two months was really a challenge for our business. In some segments, in flats, quarto, for example, the market is quite stable, but in longs we already see that a storm is coming.”

If the EU is not given an exemption from US tariffs, moreover, Italian suppliers will return to supplying the European market, Fazekas added.

Moravec said potential risks for the Czech market include reduced consumption; price volatility; the performance of Germany, on which Czech steel suppliers rely; and Chinese and Russian exports. Moreover, customers’ payment discipline could cause problems. Opportunities include digitalisation and investment into other products such as plastic or composite materials, in order to offer customers a complete package.

In a presentation earlier in the day, Moravec observed the success of populist governments in the V4 region should not have a negative impact on the recent good economic growth.

US steel tariffs should have little direct impact on European steel sellers as no EU countries are among the US’ major suppliers. The tariffs are therefore “…not critical or vital for the European industry in general,” Moravec opined. “On the other hand, there is the risk of pressure towards prices because all the countries, if they are not able to export to the USA, they will be trying to find new markets.”

Kallanish

New EU trade investigation concerns Italian stainless distributors

![]()

Italian distributors and processors of stainless steel products say that they have concerns about the ongoing EU trade investigation on possible new safeguard measures, Kallanish learns from a note issued by local association Assofermet. The measures are intended to limit the imports of ferrous products and therefore could also impact the stainless sector.

The European Commission initiated an investigation in April over possible new safeguard measures for steel. This was in response to the imposition of Section 232 import tariffs in the US and the threat of a re-direction of volumes to the EU (see Kallanish passim).

Assofermet notes that, within the stainless steel sector, new barriers would be especially harmful for the distribution segment. It calculates that Italian distributors could lose up to 30% of their turnover as a result and that stainless prices could rise immediately.

The association adds that the EU stainless steel sector already suffers from a limited internal competition due to recent consolidations both in production and distribution. “European production is also incapable of completely satisfying local demand,” Assofermet notes.

As a result, the imposition of new barriers or a quota system for the stainless steel sector would impact the distribution market significantly. This would further increase the risk of delocalisation and put the fragile recovery seen lately in jeopardy, the note concludes.

EU distribution shipments fall in first quarter

![]()

Shipments from both steel service centres (SSC) and multi-products distributors moved downwards compared with last year in the first quarter of 2018, Kallanish learns from the latest data issued by European distributors’ association EUROMETAL.

Flat steel service centres saw shipments decrease by -1.9% year-on-year in Q1 2018. When expressed in days of shipments, stocks at EU SSC averaged in March 2018 at 64 days against 60 days in March 2017. For same months, the index of stock volumes moved from 116 in March 2017 to 110 in March 2018 (average 2015 index = 100), EUROMETAL confirms.

Shipments by EU Multi-Product & Proximity Steel stockholding distributors slipped by -1.5% y-o-yin total. Long products shipments fell significantly, while shipments of coil, plate and tube saw an improvement compared with last year, says EUROMETAL without giving figures. Nevertheless, the improvement in these was not strong enough to offset the fall in longs.

The stock volumes index at EU multi-product & proximity steel stockholding distributors was 103 in March 2018, compared to 101 in the year-before period. When expressed in days of shipments, stock volumes in March 2018 levelled at 75 days, compared with 68 days in March 2017.

In comparison the market grew by 2.5% y-o-y for SSC and by 0.6% for multi-products distributors in Q1 2017, Kallanish notes.

Remaining parts of Remag sold off to Steel Mont

All operative parts of insolvent German steel distributor Remag have been sold now as the remaining parts – the distribution units in Nuremberg and Soest – have been taken over by Anaj Trade, a sister company of Indian trading house Steel Mont.

Florian Dausend, managing partner at Cornelius Treuhand, the company managing the sale of Remag, told S&P Global Platts that Steel Mont’s takeover was completed in April, but only included the flat steel part of the business. Steel Mont also has offices in Duesseldorf.

As previously reported, German distributor and rebar fabricator Suelzle acquired Remag’s Hagmeyer steel service centers in Geislingen and bending and processing works in Goeppingen, as well as its rebar distributor BTM Muenchen and the company’s Stahl Ehrenfriedersdorf site for flat and long products earlier this year.

Dausend said the diverse portfolio of the company made it difficult to sell it as a whole.

“We were flexible during the investor process and offered the group as a whole as well as single entities. The M&A process was therefore open in regards to the outcome. In that sense there has not been a target that there would be a sale as a whole only. In the end, there has not been an offer made for that,” he said.

The search for financial investors was difficult, said Dausend, as steel companies such as Remag would be currently not attractive for them.

Remag traded 200,000 mt/year of steel products and was mainly active in the southern parts of Germany.

The company applied for insolvency in October last year following uncertainties with a trade credit insurer over the credit limits that made it difficult to pursue refinancing for 2018. Market sources told Platts that due to this issue, some deals could not be done.

Laura Varriale, PLATTS

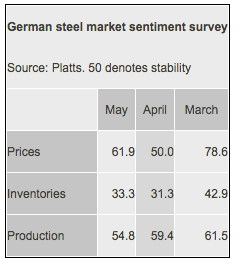

German stockists looking to destock in May: survey

German buyers are looking to stay in waiting mode as the latest monthly S&P Global Platts steel sentiment survey showed the index for inventories continuing to drop this month.

Stockholders and traders indicated they would remain hesitant about booking orders in the coming weeks. The index for that particular sector was at 8.3, indicating the intention to destock. Stockholders in particular sit on high stocks.

As reported, March levels at German stockholders stood at 1.55 million mt for flats and 878,000 mt for long products, the highest levels since July 2014.

Traders on the other hand are currently waiting for clarity over the details of expected safeguard measures by the EU on steel imports following the US Section 232 tariff announcements, while activity in the northern European import market remains subdued.

End-users expect inventories to rise, indicating they would increase purchasing this month. Overall, Platts’ index for inventories gave a reading of 33.3, significantly below the 50.0 mark that notes stability.

The pricing outlook increased to 61.9, suggesting the expectation of increasing prices. Mills and end buyers were the most bullish, while the stockholding side showed a bearish outlook at 41.7. Sources said German producers would keep prices firm for the moment.

The outlook for May production was up slightly from last month’s survey, with an overall indication of 54.8. Mills and stockholding respondents were firm in their outlook, but end users indicated they would slightly decrease output in May.

Laura Varriale, PLATTS

Polish distributor sees improved outlook, but 232 threat

![]()

The outlook for Polish economic growth in 2018 has improved from forecasts made last year, with Gdp now set to rise over 4% this year. Steel consumption, meanwhile, should grow 2-3% and 1.9% in the EU as a whole. However, US 232 steel tariffs look set to change trading patterns, which could have a negative impact on the EU market. This is according to top-three Polish distributor Konsorcjum Stali (KS).

Stable consumption should help support current steel price trends; however, 232 tariffs are a new factor that could destabilise the situation, according to KS. “The US’ protectionist trade policy could result in repercussions from other countries and lead to a trade war,” the distributor says in a report seen by Kallanish. The tariffs are “… one of the biggest threats to economic stability in the coming years.”

In 2017 KS increased sales 5% on-year to 639,000 tonnes. This was driven by a 7% rise in traded product sales to 398,000t. Rebar sales rose 15% to 168,000t, but sheet deliveries fell -6.8% to 69,000t. Z and G sections sales were flat at 60,000t. Sales of KS-produced or processed products, meanwhile, rose 3.4% to 241,000t.

Sheet deliveries nevertheless generated 17.9% more revenue at PLN 183.4 million ($51.35m) due to the gradual ramp-up of the coil service centre in Krakow, which was opened in 2013, and the resulting increase in cold and hot-dip galvanized coil processing.

Exports accounted for 0.56% of KS revenue in 2017, down from 0.58% in 2016.

Celsa Huta Ostrowiec and CMC Poland accounted for 26.2% and 19.2% respectively of KS’ procurement in 2017.

KS says the anticipated investment into developing the Polish railways and energy sector, as well as further expansion of road infrastructure and residential construction will continue to generate significant steel demand. However, Brexit will result in a reduction of EU structural and investment funding available for poorer member countries. “This could have a negative impact on the scope of investments realised in Poland after 2020, and therefore also have a negative impact on steel demand in Poland,” KS observes.

KS reported a 26% increase in revenue in 2017 to PLN 1.53 billion, but net profit fell -3% to PLN 41.55m due to higher costs.

March German stockholder inventories highest since July 2014

March German stock levels reached their highest level since July 2014, according to latest data from German stockholders’ association, BDS.

Flat steel products volumes at German stockholders and distributors went up by 3.8% year on year to 1.55 million mt in March, while long products increased by 4.82% on year to 878,000 mt — levels last seen in July 2014 when volumes reached 1.56 million mt for flat and 935,021 mt for long products.

A more detailed look at stock level changes from February to March showed that stockholders saw a re-stocking period in March.

Flat product levels rose 6.02% month on month, long products grew 2.61%. The data suggests that stocks moved up following active buying in the beginning of the year, with average lead times of four-to-six weeks for longs and six-to-eight weeks for flats depending on the specific mill. Sources told Platts that buying interest from German stockists had been limited throughout March and April amid the increased stock levels.

At the same time, sales volumes increased 9.76% month on month to 296,229 mt for longs and 3.67%to 582,090 mt for flat products. Sources of flat steel products told Platts, however, that stockists had difficulty passing margins on to customers, as offers from producers remained high.

Sales volumes compared to a year ago saw a 11.51% year-on-year drop to 296,229 mt for long products, while flat products decreased by 6.72% year on year to 582,090 mt.

Laura Varriale, PLATTS