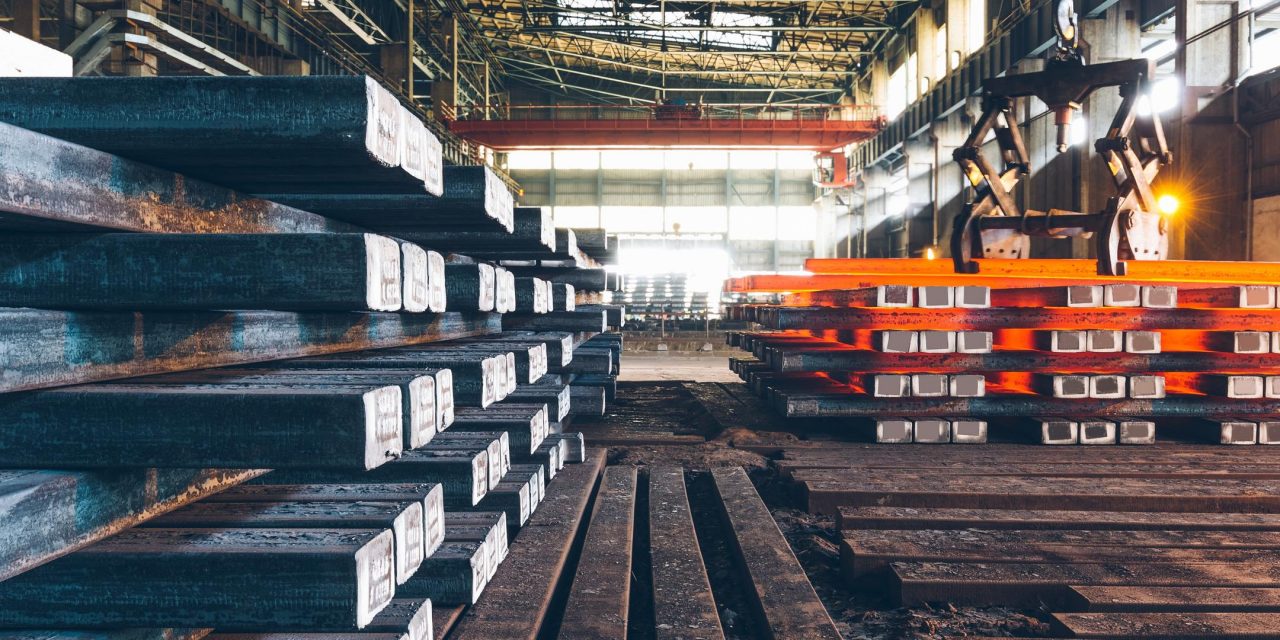

European HRC producers cut offers; trading remains slow as buyers believe bottom yet to be reached

“Buyers only book [HRC] tonnages for a short run, since prices are dropping every week. On top of sluggish demand, we are also seeing falling raw materials prices,” a source at a steel service center in the Benelux region said.

HRC offers from integrated mills in northern Europe were reported at €700-720 ($764-786) per tonne ex-works, compared to €730-750 per tonne ex-works in late February. Buyers’ estimations of tradeable values were heard at €670-690 per tonne ex-works on Friday.

April- and May-delivery coil was said to be available from local suppliers.

Sources, however, pointed out that those prices were only indicative since trading has been nonexistent in the region lately.

“There are no inquiries and hardly any bids. Buyers are waiting; they are focused on ex-stock sales instead and there is severe competition in the secondary market since demand [from end-users] remains dull,” a mill source said.

Industry sources continued to insist that production cuts could help to stop the downtrend and balance supply and demand.

As a result of the above, Fastmarkets calculated its daily steel hot-rolled coil index domestic, exw Northern Europe at €692.50 per tonne on Friday, down by €2.83 per tonne from €695.33 per tonne on Thursday.

The index was down by €11.75 per tonne week on week and by €45.10 per tonne month on month.

In Southern Europe, Fastmarkets’ corresponding daily steel HRC index, domestic, exw Italy was calculated at €671.67 per tonne on Friday, down by €2.08 per tonne from €673.75 per tonne on Thursday.

The index was down by €7.08 per tonne week on week and by €59.16 per tonne month on month.

April-delivery coil was offered by a local supplier at €690 per tonne delivered (€680 per tonne ex-works).

Rare transactions were done at lower levels of €670 per tonne ex-works. Bids were reported at €650 per tonne ex-works.

But Italian buyers were mainly only making urgent bookings to cover immediate needs and have also been postponing restocking amid bearish expectations.

“Prices [for HRC] keep falling. And, naturally, buyers want to restock when the price hits the rock bottom. So, the market remains quiet so far,” a buyer in Italy said.

Import HRC prices have also been declining amid poor demand globally and amid a downtrend in raw material prices.

Despite that, import bookings were also rare.

“No price reduction helps buyers book new [import] orders when the domestic price is sliding non-stop,” a buyer source said.

HRC offers for June- and July-arrival material from Asian suppliers were heard at €575-600 per tonne CFR on Friday.

A limited tonnage of May-shipment HRC from Saudi Arabia was offered at €570 per tonne CFR to Southern Europe.

And two sources reported an HRC offer from Turkey at €640 per tonne CFR, including the anti-dumping duty.

How is the steel industry supporting DRI expansion amid weak global demand?

Fastmarkets explores the steelmaking industry’s approach to supporting the expansion of the DRI market amid falling steel prices.

Weak steel demand across major consumption hubs in 2023

A slowdown in economic activity across major economic zones caused a dip in downstream steel prices, especially for construction-related materials.

Fastmarkets’ price assessment for steel reinforcing bar (rebar) import, cfr main EU port Southern Europe averaged €616.01 ($673) per tonne at the midpoint in 2023, down by €219.09 per tonne, or 26.24%, from €835.10 per tonne the previous year.

And Fastmarkets’ price assessment for steel hot-rolled coil import, cfr main port Turkey averaged $626.20 per tonne at the midpoint in 2023, down by $123.55 per tonne, or 16.48%, from $749.75 per tonne the previous year. 2022 prices were also down by 16.16% compared with 2021.

Tighter liquidity for construction-related projects and consumer products across Europe resulted in weak overall demand for steel in Europe in 2023, a Europe-based trader said.

The trader also expected weak consumer confidence in major economies to weigh on consumption-led demand in 2024, which could lead to a continued slowdown in steel consumption.

Annual inflation in the euro area is expected to be 2.6% in February, down by 5.9% year on year, according to Eurostat data .

The inflation rate for non-energy industrial goods is expected to be 1.6% in February, down by 5.2% year on year.

“The steelmaking industry is one of the largest markets for DRI exports from the Middle East,” a steelmaker source in the Middle East said. “A slowdown in steel prices in the regions has hampered the ability of steelmakers to procure further DRI cargoes.”

Europe imported 2.6 million tonnes of DRI in 2023, down by 11% year on year, according to Eurostat data.

Weak consumer and construction demand, alongside an influx of exports from China, caused steel prices to fall across Northeast and Southeast Asia.

Fastmarkets’ calculation of the steel reinforcing bar (rebar) index export, fob China main port averaged $596.01 per tonne in 2023, down by $113.09 per tonne, or 15.95%, from $709.10 per tonne the previous year.

Fastmarkets’ price assessment for steel hot-rolled coil (Japan, Korea, Taiwan-origin), import, cfr Vietnam similarly slipped by $118.91 per tonne, or 16.03%, to an average of $632.10 per tonne at the midpoint in 2023 from $742.01 per tonne the previous year.

The dip in HRC prices in the CFR Vietnam market was more demand-led, in line with a dip in buying interest from major importers due to a slower-than-expected recovery in economic activity across Southeast Asia, a Singapore-based analyst said.

The analyst added that while HRC import prices fared better than those for long steel products in 2023, a downtrend in prices due to weakening demand and increased supply inflow could push prices lower.

Electric-arc furnace (EAF) utilization rates in China slipped to a near three-month low in early May to around 50.4% in response to weak steelmaking margins, according to the Southeast Asia Iron and Steel Institute.

EAF operators around the region were unlikely to be able to maintain steady levels of production amid weak steel prices due to the high cost of EAF inputs — which include steel and DRI — a Shanghai-based trader said.

The trader said that the high cost of DRI as a raw material is a strong deterrent for most mills that are under cost pressure, adding that the only way to support expanded usage of DRI would be through a stronger emphasis on green premiums.

Weaker DRI consumption weighs on DR pellet premiums

Premiums for direct-reduced (DR) pellets from Vale — which are settled on the monthly basis of a 65% Fe CFR Qingdao index — averaged $51.25 per tonne in 2023, down by $22.40 per tonne, or 30.41%, from $73.65 per tonne the previous year.

Weaker demand from key regional buyers in the first half of 2024 also caused DR pellet premiums to ease further.

Second-quarter 2024 premiums for DR pellets from Vale slipped by $2 per tonne to $53 per tonne, despite a tighter pellet market in Europe following the second train derailment faced by Swedish pellet producer LKAB.

“Demand for DR pellets has been on the weaker side since the second half of 2023, mainly due to lower regional steel prices, which has affected steelmakers’ ability to use more DRI material,” a second steelmaker source in the Middle East said.

“Given the expectation of steady DR pellet supplies in the region, with an increasing pellet inventory in Oman, the need to import more DR pellets has been significantly lower compared with previous quarters,” the second steelmaker source added.

Increasing DR pellet inventory among DRI producers in the Middle East in 2023 was an indication of weaker DRI demand from European steelmakers, a Singapore-based trader told Fastmarkets.

But the trader added that DRI consumption may rebound in the second quarter of 2024, when some European steelmakers are expected to put their blast furnaces (BFs) out for maintenance.

Stronger emphasis on green steel premiums to boost DRI usability

Market participants continue to doubt the economic usefulness of DRI as a steelmaking raw material due to its higher cost compared with other BF feeds.

“On its own, it makes little sense for a steelmaker to increase their consumption of DRI when steel prices are on the low side,” a second Singapore trader said. “The value of DRI as a low-carbon raw material has been severely underplayed, especially in the past few years with falling steel prices.”

Green premiums have taken a backseat in recent years due to the slowdown in economic growth, which has inherently affected prices for low-emission raw materials, a second trader based in Europe said.

A stronger price distinction between “green” steel and regular steel could translate into stronger demand for low-carbon materials such as DRI. This could have the impact of shaping the market structure into one that adds more value to low-emission products, Fastmarkets understands.

Fastmarkets’ green steel domestic, flat-rolled, differential to HRC index, exw Northern Europe averaged €200 per tonne in the first two months of 2024, up by €19.23 per tonne, or 10.64%, from €180.77 per tonne in the fourth quarter of 2023.

Further regulations over carbon tracking to establish tangible economic value on DRI use

Most market participants believed that stiffer regulatory support is required to expand the use of low-carbon raw materials against headwinds in the steelmaking industry.

Major steelmaking hubs in Asia — such as China, India and Southeast Asia — need to keep up with their regulatory controls on carbon reporting among steelmakers, a third trader in Singapore said.

The trader added that tighter carbon reporting controls from major importers of Asian steel could prompt the governments of the various steelmaking hubs to establish tighter carbon controls.

“Carbon reporting essentially places a stronger emphasis on the value of raw material inputs, adding value to raw materials that generate a smaller carbon footprint in production,” a Singapore-based analyst said.

“Tougher carbon reporting systems provide a necessary support for green steel premiums, incentivizing the use of DRI as a raw material across more steelmaking hubs,” the analyst added.

China’s National Development and Reform Commission (NDRC) announced on November 22 that it would establish a carbon footprint management system to promote the labeling of carbon products.

The ramp-up in carbon labeling is in line with the establishment of accounting and evaluation systems for the carbon footprint of major imports, including steel products, the NDRC added.

Chinese premier Li Qiang also signed additional regulations against Chinese industrial producers found to be falsifying data on emissions reductions on February 4.

CBAM as a means to reshape production norms in steelmaking

The EU’s Carbon Border Adjustment Mechanism (CBAM), expected to be fully implemented from 2026 onward, is a regulatory framework used to put a fair price on the carbon emitted in the production of imports into the EU, according to the European Commission.

EU importers will declare the emissions embedded in their imports — which include steel cargoes — and surrender the corresponding number of CBAM certificates, which are procured through a weekly average auction.

If importers can prove that a carbon price has already been paid during the production of the imported goods, the corresponding amount can be deducted.

The CBAM framework essentially levels the competitive advantages of imported steel with domestically produced steel in Europe by putting penalties on carbon emissions, according to a third source in the Middle East.

The source added that the CBAM framework incentivizes steel imports that are produced using low-carbon raw materials such as DRI, nudging steelmakers toward EAF steelmaking methods and increasing DRI consumption.

The EU is the largest net importer of steel cargoes in the world, importing around 22 million tonnes of steel in 2022, 1.4 million tonnes higher than the US.

“Based on the volume of its steel imports, the EU has the strongest potential to support DRI premiums in the medium term with its approach of back-tracing carbon emissions,” a fourth trader in Singapore said.

“But industrial-wide efforts from major steelmaking hubs such as the Middle East will remain paramount in supporting the continued expansion of the DRI market,” the trader added.

The MENA region’s potential as a production hub to boost DRI accessibility

Market participants are identifying the Middle East-North Africa (MENA) region as a key area with a strategic opportunity to scale up DRI production and sales.

Ample natural gas supplies, alongside its strategic geographical location servicing demand centers for green steel in Europe and key growth markets in India and Southeast Asia, make the MENA region a natural DRI hub, an analyst in the Middle East said.

The MENA region remains the largest DRI production hub in the world, contributing nearly 46% of total global production, with 58.48 million tonnes produced in 2022.

A total of 20 million tonnes per year of DRI capacity is expected to come online in the MENA region between 2024 and 2027 across hubs in Oman, Saudi Arabia and Algeria, according to a source in the region.

An expansion of DRI modules and EAFs in the MENA region has the potential to conventionalize the use of DRI as a raw material in steel production, by narrowing the production-cost gap of DRI with other raw material alternatives, the analyst in the Middle East said.

The analyst added that the long-term goal is for the MENA region to focus on hydrogen-based reduction for DRI production, to truly move the industry away from its carbon-intensive practice.

Voestalpine to sell German special steel unit

Buderus is part of voestalpine’s High Performance Metals division. Following its divestment, the division will concentrate its product portfolio on the high-tech segment of special materials, and reduce the production share of tool steel and engineering steel in the standard grade area. The resulting optimisation of the product portfolio will strengthen the High Performance Metals division’s competitive position, management believes.

In the Automotive Components unit – part of the Metal Forming Division – voestalpine is maintaining its internationalisation strategy. However, it will make targeted adjustments in response to the structural underutilisation of capacity in the automotive supply industry in Germany. Management has already responded by consolidating the production network, including the sale of the production site in Nagold, Germany, it says.

The above-mentioned measures will result in negative one-off effects on the group’s Ebitda of about €90 million ($98m) and on Ebit of about €410m, Kallanish understands. This means an adjustment to the Ebitda expectation for the business year 2023/24 from around €1.7 billion to around €1.6 billion.

In terms of other customer sectors targeted, the group notes that significant progress has been made, for example, in the area of automated warehouse technology. The promising railway infrastructure segment is also continuously expanding through strategic investments, it adds.

Christian Koehl Germany

![]()

OEMs ready for green steel, consumers resist: conference

“In the near term, I do not see the possibility to offer green steel without a price premium,” Eike Brünger, sales director at Salzgitter AG, said in an interview session. “However, I do imagine that green steel at some point will become the standard, and from that point will benefit from a cost effect in large-scale production.”

The other interviewee in that session, Gunnar Gütheke of Mercedes Benz, questioned the willingness of the consumer to pay more for a car. “Currently, the prices paid for cars are actually declining,” he noted. “Customers want a competitive and sustainable product, and we are working on offering this in a cost-neutral way.”

After all, the sustainability of a car is not confined to the steel used in it, Gütheke replied when the moderator asked how the company takes the “greenness” into its calculation. “We are breaking the calculation down to components,” he said, adding that the company aims to be able to offer cars with a zero-carbon footprint by 2039.

Another speaker, Guido Kerkhoff of steel distribution group Klöckner & Co, said the premium for green steel plays a negligible role in the finished product price. “Even if the steel price went up by 50%, the price for a passenger car would rise by a mere 0.7%,” he opined.

Christian Koehl Germany

![]()

Biden says US Steel must remain ‘domestically owned’

US president Joe Biden has issued new comments that are interpreted as more directly opposing the acquistion of US Steel by Japan’s Nippon Steel, Kallanish reports.

In a White House statement on Thursday, the president expresses concern about foreign ownership of a vital industrial enterprise and the impact on employees. Earlier Biden had promised a thorough review of the proposed acquisition, which the two iconic steelmakers announced in December (see Kallanish passim).

“It is important that we maintain strong American steel companies powered by American steel workers,” proclaims Biden now. “I told our steel workers I have their backs, and I meant it. US Steel has been an iconic American steel company for more than a century, and it is vital for it to remain an American steel company that is domestically owned and operated.”

The United Steelworkers (USW) labour union reacted very positively to the latest White House statement. The USW preferred an earlier takeover offer from domestic competitor Cleveland-Cliffs.

“Allowing one of our nation’s largest steel manufacturers to be purchased by a foreign-owned corporation leaves us vulnerable when meeting our defence and critical infrastructure needs,” the union emphasises in a statement of its own on Thursday.

A US flat-steel purchaser tells Kallanish that he would not favor a sale of US Steel to Nippon, but the source further argues that a takeover by Cleveland-Cliffs might be even worse for the customers.

“I would really have liked to see Steel Dynamics or some other domestic steelmaker bid. We can’t have Cliffs responsible for that much of the market. It’s too much control for them,” states the steel buyer.

Under the terms of its basic labour agreement with US Steel, the USW awarded Cleveland-Cliffs a right-to-bid assignment for the 123-year-old Pittsburgh, Pennsylvania-based company in August 2023. US Steel management rejected an unsolicited $7.3 billion buyout proposal from its Cleveland, Ohio-based rival that same month (see Kallanish 15 August 2023).

Biden’s latest remarks arrive ahead of an April visit from the prime minister of Japan, Fumio Kishida.

Technically, the Nippon acquisition agreement provides that US Steel operations would be, in effect, held by a now-small US subsidiary named NIppon Steel North America, based in Houston, Texas (see Kallanish 17 January). The USW has criticised the arrangement. Neither of Thursday’s statements directly addresses that nuance.

Kristen DiLandro USA

![]()

Weak demand inhibits trading in Northern European long steel market

Fastmarkets’ weekly price assessment for steel reinforcing bar (rebar), domestic, delivered Northern Europe, was €645-660 ($705-722) per tonne on Wednesday, down by €5 per tonne from €650-665 per tonne week on week.

Weak trading resulted in ongoing bearish sentiment in the Northern European rebar market, sources said.

“There is no demand either for domestic or imported stock,” a buyer source in Germany said.

Fastmarkets’ calculation of its daily index for steel scrap HMS 1&2 (80:20 mix) North Europe origin, cfr Turkey was $377.51 per tonne on Wednesday, up from $373.83 per tonne week on week.

Meanwhile, the corresponding Fastmarkets’ weekly price assessment for steel wire rod (mesh quality), domestic, delivered Northern Europe was €645-660 per tonne on Wednesday, stable week on week.

IREPAS

Weak consumption from the construction industry has continued to inhibit trading in the European long steel market, according to the short-range outlook published by the International Rebar Producers and Exporters Association on March 5.

“The EU market is very quiet as residential construction has declined substantially in northern Europe. There is very little activity and prices from domestic mills are as stable as a rock. There is some increase in imports including unusual origins such as China, Oman and the [United Arab Emirates]. Other sources are not able to compete with domestic offers,” the report said.

However, a softening of raw materials could take lower cost pressure on mills, the report added.

“In Europe, the slow economy has reduced ferrous scrap flow and also demand from the steel industry which is struggling with poor order books. The only good news for steel mills nowadays could be that the raw material prices, both for iron ore and scrap, are going down. Also, lower activity means lower volumes, reducing supply pressure on the markets,” the outlook added.

HRC prices little changed in Europe amid ‘non-existent’ trading

“There is no pick-up in trading. Lowering prices failed to spur steel demand. Buyers just keep purchasing hand-to-mouth, expecting prices to drop more tomorrow,” a buyer in Germany said.

Buyers were not interested in replenishing stocks due to lower order intake from end users, Fastmarkets understands.

Besides, industry sources expected domestic HRC prices to keep sliding in the short term, with a downtrend in raw materials prices adding pressure to already weak finished steel markets.

“Mills are hungry for orders but at the same time not prepared to cut prices significantly,” a buyer source in Northern Europe said. “[End-user] demand is also very weak; therefore, most buyers don’t feel the need to restock.”

Sources pointed out that buyers were destocking, with tough competition in the secondary market among steel service centers, traders and stockists.

Northern European steelmakers were reportedly trying to keep offers at €700-730 ($766-798) per tonne ex-works, while buyers’ ideas of achievable prices were heard at €680-700 per tonne ex-works.

Mills in Northern Europe were heard offering April-May lead times.

Fastmarkets calculated its daily steel hot-rolled coil index domestic, exw Northern Europe at €695.33 per tonne on Thursday, down by €0.92 per tonne from €696.25 per tonne on Wednesday.

The index was down by €12.80 per tonne week on week and by €50.67 per tonne month on month.

In Southern Europe, Fastmarkets’ corresponding steel hot-rolled coil index domestic, exw Italy was calculated at €673.75 per tonne on Thursday, down by €1.25 per tonne from €675.00 per tonne on Wednesday.

The index was down by €13.75 per tonne week on week and by €61.88 per tonne month on month.

In Italy, low tonnages of HRC were reported traded around €670 per tonne ex-works, with buyer estimates of achievable prices at €650-680 per tonne ex-works.

April-delivery HRC was still available from Italian suppliers, Fastmarkets understands.

Buyers said that the bottom for HRC prices in Italy has yet to be reached, so they were in no rush to make any bookings.

“There is still room for [HRC] price correction. The only efficient way to stop the downtrend would be output cuts, but European mills are not in a hurry to implement those,” a buyer in Italy said.

HRC offers for June-July arrival from Taiwan, Vietnam and Japan were heard at €580-600 per tonne CFR on Thursday.

But buying interest in import coil was also limited, despite prices being lower than domestic ones, Fastmarkets understands.

EU import safeguard risks were high, especially for the “other countries” category, where the cheapest offers come from — namely Vietnam, Japan and Taiwan — and lead times were quite long, sources said.

Buyers also expected import prices to sink even lower in the short term due to poor demand and sliding raw material costs, sources said.

Southern European steel longs prices stable; IREPAS outlook remains bleak

Fastmarkets price assessment for steel reinforcing bar (rebar) domestic, exw Italy was €625-645 ($684-705) per tonne on Wednesday, down by €5 per tonne week on week from €630-650 per tonne.

Minimal buying appetite and a bearish outlook resulted in weak trading in the Italian rebar market during the week, sources said.

“The minimum price is a little lower than last week, as the market is still flat,” a buyer source in Southern Europe said.

“Rebar seems to edge down every week as mills don’t seem to be able to sustain prices or increase them. And demand remains low as bad weather has slowed construction,” a second buyer source said.

“I would say prices are stable but with very limited volumes. We have had 10 days of almost constant rain, so many major construction sites are closed,” a producer source said.

“Scrap prices have not been lowering as quickly as expected, so I think producers will soon have to push for increases, hopefully aided by better weather and higher demand as construction projects related to Italy’s National Recovery and Resilience Plan try to catch up for lost time,” the producer source added.

Fastmarkets’ calculation of its daily index for steel scrap HMS 1&2 (80:20 mix) North Europe origin, cfr Turkey was $377.51 per tonne on Wednesday, up week on week from $373.83 per tonne.

And Fastmarkets’ price assessment for steel reinforcing bar (rebar) domestic, delivered Spain was €625-645 per tonne on Wednesday, down by €5 per tonne week on week from €630-650 per tonne.

Southern European wire rod

Fastmarkets’ price assessment for steel wire rod (mesh quality) domestic, delivered Southern Europe was €640-650 per tonne on Wednesday, narrowing downward by €5 per tonne week on week from €640-655 per tonne.

IREPAS

Weak consumption from the construction industry has continued to inhibit trading in the European long steel market, according to the short-term outlook published by the International Rebar Producers and Exporters Association (IREPAS) on March 5.

The outlook for future demand remained bleak.

“The current status of the market can be described as unstable in many markets or stable at a low level at best. The outlook, unfortunately, is slow and unsatisfactory,” the report said.

But lower raw materials prices could reduce cost pressure on mills, according to the IREPAS report.

“In Europe, the slow economy has reduced ferrous scrap flow and demand from the steel industry, which is struggling with poor order books. The only good news for steel mills nowadays could be that the raw material prices, both for iron ore and scrap, are going down. Also, lower activity means lower volumes, reducing supply pressure on the markets,” the report said.

Klöckner expects increased sales in 2024

The steel distribution group therefore anticipates increased shipments and sales over 2023. The outlook it gives for specific industries in its main regions sounds somewhat more modest, though.

For North America, the German-based steel distributor forecasts growth of between 1% and 3%, with slight growth seen for the construction and energy industries. Transportation sectors – encompassing cars, shipbuilding, trains – mechanical engineering and white goods are seen on par with the previous year.

For Europe, it expects a growth of only 0-1%, with a slight upward trend for energy and white goods, while the other sectors are seen remaining flat.

In 2023, Klöckner’s shipments were 4.25 million tonnes, a slight increase from the 2022 volume of 4.19mt achieved in 2022. The increase was mainly driven by the “strong development” of Kloeckner Metals Americas, Kallanish learns from the group’s annual results presentation. Revenue, however, fell by 17% to €6.96 billion ($7.3 billion), due to the considerably lower price levels compared with 2022.

The net result from continuing operations was close to breakeven, with a net loss of €0.3 million. However, impairment losses in connection with discontinued operations – meaning the sale of the country organisations of France, the United Kingdom, the Netherlands and Belgium – meant Klöckner ended up with a net loss of €190m.

Christian Koehl Germany

![]()

Negative sentiment, lower prices impact Italian scrap: Assofermet

Sources are reporting continued lower scrap collection, as well as great uncertainty. This “has somewhat delayed the closing of contracts in these first days of March. The reason for this uncertainty is mainly due to the trend of lower sales of finished products, which has not improved, forcing steelmakers to partially review production programmes,” the note says.

February recorded mostly stable scrap prices, without major variations, while steel production slowed towards the end of January. Despite the weaker scrap collection, stocks at several scrap yards were low and prices remained unchanged. In the last days of February, some steelworks, especially in the Brescia area, limited scrap deliveries.

Italian scrap prices are decreasing this month after a period of lull by €20/tonne, or $21.8/t (see Kallanish 13 March).

Meanwhile, the association sees declining pig iron prices in March, in line with weaker finished product prices. Brazilian pig iron levels towards the US market are flat on-month. while a slowdown in pig iron purchases has been recorded on the Turkish market. Assofermet notes a decrease in Russian pig iron volumes on the Chinese market, mainly due to hiking freight rates from the Black Sea, which makes the Chinese market unattractive for Russian suppliers.

“In February, the pig iron market in Italy remained substantially unchanged. There were no price reductions but there was a decline in demand. Availability remains good, although not excessive,” Assofermet concludes.

Natalia Capra France

![]()