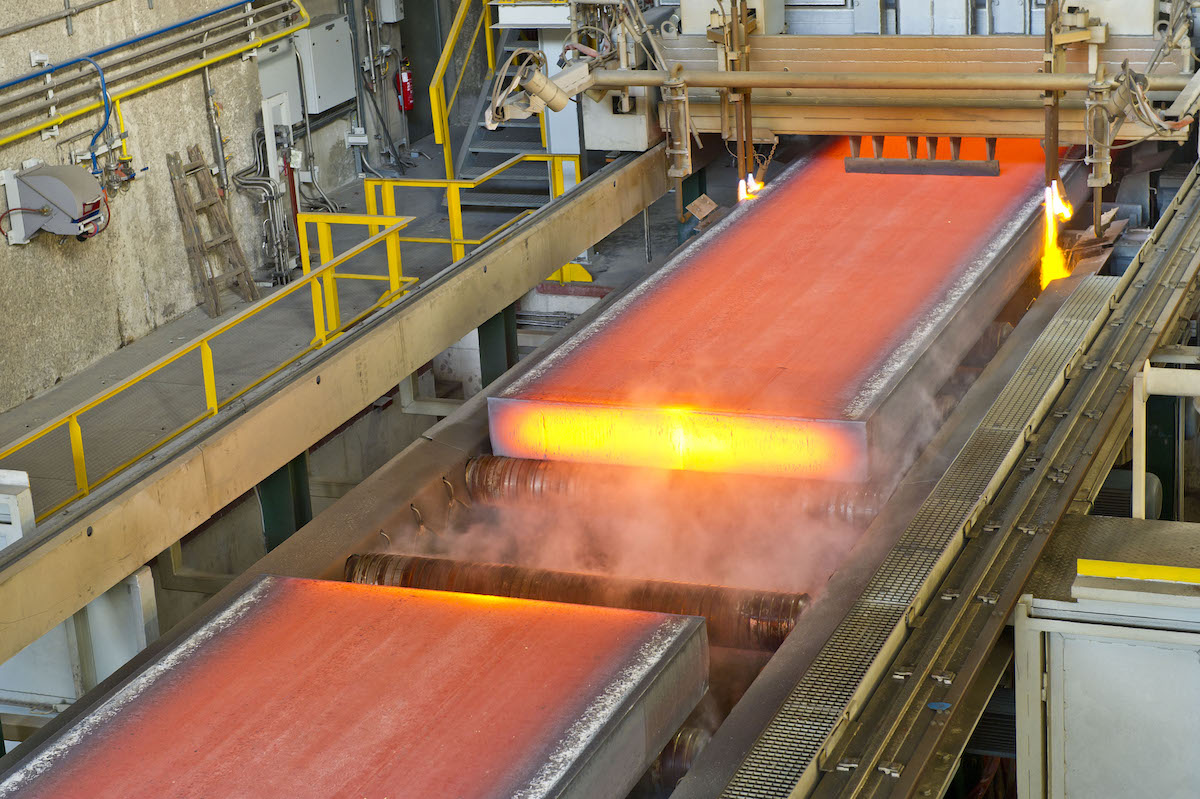

European Commission investigates extending steel safeguard quotas

The European Commission initiated a review into a possible extension of safeguard quotas on steel imports into the European Union, according to a notification in the Official Journal Feb. 9.

According to the EC, 14 EU member states sent a request to extend the tariff-rate quotas to 2026.

“The request contains sufficient evidence suggesting that the safeguard measure continues to be necessary to prevent or remedy serious injury and that Union producers are adjusting,” the EC said.

As part of the extension investigation, the EC will review the allocation of tariff rate quotas, products as well as categories. The deadline for feedback is Feb. 26.

Market participants mostly welcomed the investigation Feb. 9.

“We need the safeguard extension,” an Italian flat steel service center source said. “Otherwise imports would flood the European market, and the prices would collapse. Neither mills nor distribution need the removal of safeguard.”

European market participants have been warning of the redirection of trade flows while the US is holding up its section 232 measures on imports as European producers are making costly technical changes at steel plants to decarbonize.

“The mills need the steel prices to remain higher to cover the costs of green transition, and exposure of the European market to import without safeguard would make it more challenging,” a European flat steel mill source said.

One European long steel buyer hoped for an update of specific country quotas.

In the current quota period, running from Jan. 1 to March 31, the hot-rolled coil as well as the wire rod other country quotas were exhausted swiftly after opening Jan. 3. The country-specific quota for hot-dipped galvanized coil for automotive use was also exhausted swiftly. Other steel import quotas remain open as of Feb. 9.

“The safeguard is a legitimate and indispensable tool for stabilizing the EU steel market and ensure the sustainability of the European steel industry, which is on its way to decarbonisation,” Axel Eggert, director general of the European Steel Association, or Eurofer, said Feb. 9.

“Massive, market-disruptive import surges from third countries, mostly with little or no climate ambition, further jeopardize the transition,” Eggert said.

Eurofer particularly warned of excess capacity being directed toward Europe without safeguard quotas, as particularly in Southeast Asia, the Middle East, and North Africa steel production is increasing, while China was close to record steel exports in 2023.

“Consequently, the European Union has become a primary target for trade deflection, with steel exports increasingly redirected towards its market,” Eurofer said.

The UK, which has set up its own steel safeguard quotas, is also investigating extending its safeguards while reviewing a temporary extension of the HRC import restrictions for nine months as Tata Steel UK will idle its two blast furnaces this year and not produce HRC until its electric arc furnace starts 2027.

Authors: Laura Varriale, laura.varriale@spglobal.com, Maria Tanatar, maria.tanatar@spglobal.com, Rabia Arif, rabia.arif@spglobal.com

EU carbon values under pressure on recession, demand worries

Sentiment in the European carbon price market remained bearish in the week to Feb. 2 amid muted demand. Traders and analysts have said they expect prices to remain around Eur60-65/mtCO2e in the coming week, with macroeconomic concerns and reduced power generation dominating headlines.

EU Allowances under the bloc’s Emissions Trading System were trading at Eur63.22/mtCO2e at 1038 GMT on Feb. 2 compared with Eur63.58/mtCO2e on Jan. 26.

Platts, part of S&P Global Commodity Insights, assessed EUA contracts for December delivery at Eur62.19/mtCO2e on Feb. 1.

Many analysts have downwardly revised their EUA price forecast for 2024 due to recession concerns and reduced emissions from the power and industrial sectors.

Analysts at S&P Global expect 2024 average prices to plunge to Eur63.90/mtCO2e compared with Eur85.30/mtCO2e in 2023 and Eur81.50/mtCO2e in 2022.

“EUA prices are expected to decline further due to the expectation of a technical recession despite a resilient labor market,” they said in a recent note. “The slowdown is broad-based affecting sectors like construction, manufacturing, and services. We expect prices to hit the high Eur50/mt mark threshold in February.”

Climate reforms

On Feb. 6, the European Commission is likely to recommend that the EU commit to a 90% reduction in emissions by 2040, which could provide some relief to declining prices.

This target is being backed by several EU countries, but climate policies have become heavily politicized recently, with farmers across Europe currently protesting against costly clean energy regulations.

But many policymakers, analysts and climate scientists insist that the EU must commit to this if it has any realistic chance of reaching net zero by 2050.

The European Council has set a goal for the EU to cut its greenhouse gas emissions by at least 55% by 2030, compared with 1990, and become climate neutral by 2050.

Meanwhile, the inclusion of the maritime sector in the EU ETS, opens up a new set of buyers for EUAs.

The European Commission published a document Jan. 31 attributing each shipping company to an EU member state to help these companies register for EU ETS compliance.

Shipping companies can now open holding accounts to trade EUAs and manage their ETS exposure.

Under the EU ETS guidelines, shipping companies must surrender their first ETS allowances by Sept. 30, 2025, for emissions reported in 2024.

The EU has also agreed on a phase-in period to give the industry some preparation time, with the ETS covering 40% of the emissions in 2024, 70% in 2025 and 100% from 2026 onward.

The shipping sector’s inclusion is projected to add emissions of 90 million mtCO2e this year, which is around two-thirds of the sector’s emissions.

CBAM extension

Meanwhile, the European Commission extended has the period for declarants to submit their quarterly reports under the Carbon Border Adjustment Mechanism by 30 days from the original deadline, after a significant number of importers experienced technical issues that led to some businesses being unable to make submissions.

The new carbon border tax entered into application in a transitional phase Oct. 1, with the first reporting period for importers originally set to end Jan. 31.

CBAM essentially levies a tax on imports of selected carbon intensive materials and products (including aluminum, cement, electricity, fertilizers, hydrogen, iron and steel) into the EU, removing the gap between the EU ETS carbon price and the export country of origin’s carbon price.

The main purpose of the tax is to reduce the risk of carbon leakage — as a result of EU industries locating abroad — and encourage importer nations to introduce their own carbon markets and, so, limit CBAM impacts on their traded goods.

No penalties will be imposed on reporting declarants experiencing difficulties in submitting their first CBAM report, the commission said.

“While the system has been working well in previous days with data and many reports being submitted successfully, technical teams are working around the clock to rectify remaining issues,” the EC said.

The commission has encouraged those reporting declarants that do not encounter any major technical issues to submit their CBAM report by the end of the reporting period.

Author: Eklavya Gupte, eklavya.gupte@spglobal.com

Commission adopts detailed reporting rules for the CBAM’s transitional phase

On 17 August 2023, the European Commission adopted the rules governing the implementation of the Carbon Border Adjustment Mechanism (CBAM) during its transitional phase, which starts on 1 October 2023 and runs until the end of 2025.

The Implementing Regulation details the transitional reporting obligations for EU importers of CBAM goods, as well as the transitional methodology for calculating embedded emissions released during the production process of CBAM goods.

In the CBAM’s transitional phase, traders will only have to report on the emissions embedded in their imports subject to the mechanism without paying any financial adjustment. This will give adequate time for businesses to prepare in a predictable manner, while also allowing for the definitive methodology to be fine-tuned by 2026.

To help both importers and third country producers, the Commission also published today guidance for EU importers and non-EU installations on the practical implementation of the new rules. At the same time, dedicated IT tools to help importers perform and report these calculations are currently being developed, as well as training materials, webinars and tutorials to support businesses when the transitional mechanism begins. While importers will be asked to collect fourth quarter data as of 1 October 2023, their first report will only have to be submitted by 31 January 2024.

Ahead of its adoption by the Commission, the Implementing Regulation was subject to a public consultation and was subsequently approved by the CBAM Committee, composed of representatives from EU Member States. One of the central pillars of the EU’s ambitious Fit for 55 Agenda, CBAM is the EU’s landmark tool to fight carbon leakage. Carbon leakage occurs when companies based in the EU move carbon-intensive production abroad to take advantage of lower standards, or when EU products are replaced by more carbon-intensive imports, which in turn undermines our climate action.

For more information

Guidance and resources for EU importers and non-EU producers of CBAM goods

Further information on the CBAM can be found here.